Code for Machine Learning for Trading, 3rd edition — from data sourcing to live execution.

19.7k

Stars

5.4k

Forks

1

Open issues

14

Contributors

AI Analysis

This is a comprehensive code repository and educational resource for the third edition of 'Machine Learning for Trading,' covering the complete workflow from data sourcing through live strategy execution. It serves practitioners, researchers, and students in quantitative finance who want to build, backtest, and deploy ML-driven trading strategies; it is NOT a general-purpose ML library but rather a specialized educational and reference implementation for algorithmic trading workflows.

Inferred from signals mentioned in the README (tests, CI, type safety) — not a review of the actual code.

AI's overall editorial judgment — not an average of the bars above, can weigh other factors too.

Comprehensive ML-for-trading code companion evolves into a full end-to-end production curriculum

This repository is the official code companion to Stefan Jansen's 'Machine Learning for Trading' book (3rd edition), covering the entire quant workflow from data sourcing through feature engineering, model training, backtesting, and live execution. It targets quantitative finance practitioners, algorithmic traders, and advanced students who want to bridge academic ML with real trading systems. With nearly 20k stars and active maintenance as of mid-2026, it is one of the most widely referenced applied ML-in-finance resources publicly available.

Created in May 2018 alongside the first edition of the book, it has gone through at least three major revisions tracking the book's editions, each expanding scope — the third edition adds generative AI, causal ML, and full MLOps coverage.

Growth has been driven by the book's commercial success and a loyal community of quant traders and finance-focused ML practitioners. The 3rd edition relaunch in 2025-2026 with new content (LLMs, multi-agent systems, live cohort courses) likely accelerated star growth. The 159 stars in the past 7 days relative to current date suggests sustained, healthy organic growth rather than a viral spike.

Direct production trading usage of this repository's code is not verified — it is primarily educational. However, the companion website (ml4trading.io) lists six production Python libraries and live cohort courses, suggesting some users do carry the workflow into live systems. Real-world adoption in the sense of practitioners learning from and adapting this code is strongly implied by 5,345 forks and book sales, but cannot be independently confirmed.

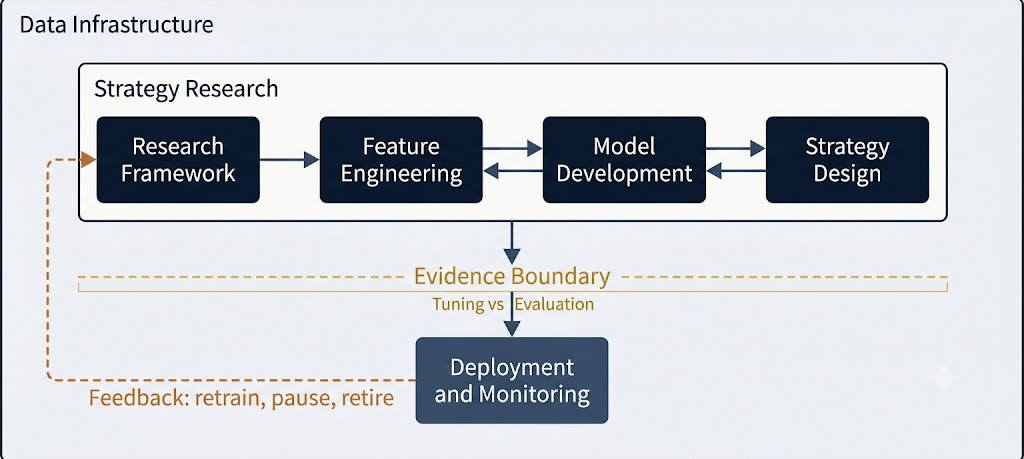

Appears to be organized as a collection of Jupyter Notebooks structured chapter-by-chapter, likely following the book's 27-chapter layout across nine case studies. Based on README, each case study runs a consistent pipeline from data ingestion to deployment. Docker environments are mentioned for reproducibility, suggesting containerized per-chapter or per-case-study setups. The tech stack appears to include Polars, PyTorch, LightGBM, Optuna, and Plotly, with integrations for Interactive Brokers, Alpaca, and QuantConnect for live trading.

Not documented in README. As a notebook-based educational repository, formal unit test coverage is unlikely to be a primary concern, though Docker reproducibility partially mitigates environment consistency issues.

Last push was 2026-06-23, six days before the evaluation date — indicating active, ongoing maintenance. The README references live courses scheduled for June 24, 2026, confirming the project is actively supported and not in maintenance-only mode. Consistent updates across an 8-year lifespan with three major edition cycles demonstrate sustained commitment.

ADOPT IF: you are learning to apply ML to quantitative trading and want a structured, end-to-end curriculum backed by a commercially published book with reproducible environments and live community support. AVOID IF: you need a production-ready, installable library rather than a learning resource — this is educational code, not a maintained software package. MONITOR IF: you are evaluating whether the live trading integrations (IBKR, Alpaca, QuantConnect) and MLOps chapters are mature enough to serve as templates for real deployment, as that evidence is not yet independently verified.

Independent dimensions

Mainstream potential

4/10

Technical importance

8/10

Adoption evidence

6/10

- As a book companion, code quality and maintenance are tied to the author's personal bandwidth and publishing cycle — a long gap between editions could leave parts of the codebase stale relative to rapidly evolving libraries like PyTorch or LightGBM.

- Jupyter Notebook-heavy repositories are inherently harder to modularize, test, and maintain than library code; learners may struggle to adapt notebook code into production systems without significant refactoring.

- The scope expansion into generative AI, causal ML, reinforcement learning, and MLOps in one resource risks becoming too broad for any single practitioner to absorb, potentially diluting the depth on core topics.

- Live trading integrations (Interactive Brokers, Alpaca) depend on third-party APIs that change without notice; notebook-level code for live execution may lag API changes and produce subtle failures for users who deploy without careful validation.

- The educational framing means there is no SLA, issue-response guarantee, or versioned release contract — users building on this code assume all maintenance and adaptation risk themselves.

Likely to remain one of the most referenced applied ML-in-finance learning resources for at least 2-3 more years, with continued growth tied to new course offerings and edition updates. Mainstream breakout beyond the quant niche is unlikely.

Newsletter

Get analyses like this every Monday

Free weekly digest of the most interesting open-source discoveries.

Languages

Information

- Website

- https://ml4trading.io

- Language

- Jupyter Notebook

- License

- MIT

- Last updated

- 2d ago

- Created

- 99mo ago

- Analyzed with

- anthropic/claude-haiku-4-5

Stars over time

Contributors over time

Top 100 contributors only — repos with more will plateau at 100.

Open issues

No open issues — clean slate.

Top contributors

Similar repos

harvard-edge/cs249r_book

A comprehensive open-source textbook and courseware repository on machine...

trekhleb/homemade-machine-learning

A comprehensive collection of popular machine learning algorithms implemented...

| Repository | Stars | Week Δ | Language | Score | Updated |

|---|---|---|---|---|---|

|

stefan-jansen/machine-learning-for-trading

this

|

19.7k | +129 | Jupyter Notebook | 8/10 | 2d ago |

|

harvard-edge/cs249r_book

|

27.2k | — | Python | 8/10 | 5d ago |

edtechre/pybroker edtechre/pybroker

|

3.4k | — | Python | 7/10 | 2mo ago |

|

trekhleb/homemade-machine-learning

|

24.6k | — | Jupyter Notebook | 8/10 | 8mo ago |

microsoft/ML-For-Beginners microsoft/ML-For-Beginners

|

87.9k | — | Jupyter Notebook | 9/10 | 1w ago |

Those are execution/backtesting frameworks; this repo is a learning curriculum with code. They are complementary rather than competing — this repo may actually teach users how to integrate those tools.

General-purpose ML education without any trading focus. Broader audience but shallower on domain-specific application. Less relevant for practitioners wanting finance-specific workflows.

Much broader audience and beginner-focused. Higher star count reflects mass appeal, not domain depth. Not a substitute for practitioners needing backtesting, factor models, or execution logic.

MlFinLab is a Python library implementing financial ML techniques. More directly usable as a dependency but less pedagogically structured. This repo teaches the 'why'; mlfinlab provides the 'what' as a package.

Narrower scope focused on stock analysis pipelines rather than the full ML research-to-deployment workflow. Less comprehensive on model variety and MLOps coverage.